From checking your policies for gaps in coverage to looking for ways to lower your premiums, there are various insurance-related tasks you should take care of heading into fall. Your fall season insurance preparation should also include comparison shopping to find out which insurer can offer you the best deal on the coverage you need.

Read below for a comprehensive insurance checklist for the fall season, including insurance review tips for the coverage types you need to protect against common autumn hazards.

|

Key Takeaways

|

1. Review Your Insurance Policies

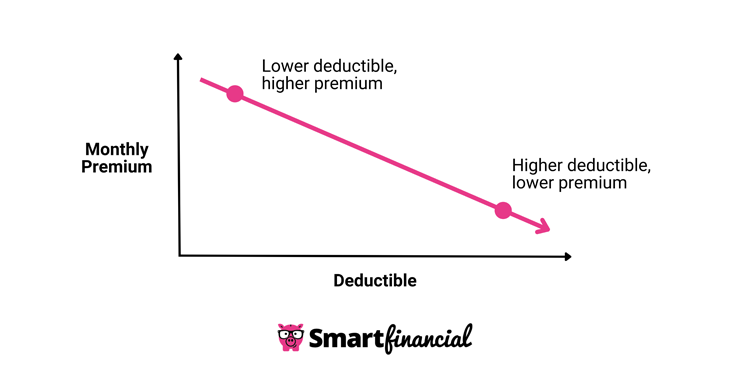

During your fall insurance preparation, you should review your current policies to evaluate whether your premiums fit within your budget and whether you have the right amount of coverage. No matter how useful an insurance coverage type could potentially be, you may be overinsured if the premiums create a significant financial strain or force you to cut other important expenses.

One way to keep your insurance prices manageable is to drop unnecessary coverage types from your policies. For example, if you have an older car that is fully paid for, you can likely cancel your physical damage auto insurance as long as the vehicle is worth less than 10 times the amount you pay for coverage.[1]

You should also check the updated value of your covered property to see if your insurance coverage limits have kept pace with inflation. Similarly, you may need to raise your coverage limits if you’ve obtained new, valuable property since your last insurance review. Maintaining a home inventory is a useful way to track the value of your most important personal belongings and determine whether you need more personal property coverage.

2. Assess Your Insurance Needs

Your insurance coverage needs can change over time, so it’s important to consider whether your current insurance policies adequately account for the risks you face in your day-to-day life. For example, if you recently started driving for Uber or a similar service, you may need to add a rideshare insurance endorsement to your car insurance to fully cover the risks associated with your work.

Changes in your circumstances may also open up opportunities for you to scale back your insurance coverage. For example, if you operate a business that recently went fully remote, you may be able to trim down your general liability coverage limits since there is no longer a risk of someone getting injured on the premises of your business.

It’s particularly important to evaluate whether your health care needs have changed before open enrollment begins on the Health Insurance Marketplace on Nov. 1.[2] For example, if you have developed a chronic illness that necessitates frequent treatments, you may want to switch to a higher-tiered plan that will cover a greater percentage of your medical costs.

3. Update Your Beneficiaries

While life insurance can sometimes feel like a “one-and-done” purchase, there are times when it may make sense to update the beneficiaries who are supposed to receive a payout if you die while the policy is active. For example, if you get divorced and remarried, it may make sense to remove your former spouse from your policy and add your new spouse as a beneficiary instead.

You should also consider adding contingent beneficiaries who can claim a death benefit if your primary beneficiaries are not available to claim it. For example, if your child has started a family since you last updated your life insurance coverage, you may want to add their spouse and children to the policy as contingent beneficiaries — that way, your child-in-law and grandchildren can still benefit from your policy, even if your child dies before you.

4. Compare Rates

Every insurance company has its own underwriting formulas that it uses to calculate risk, so it’s important to compare quotes from three to five different insurers before settling on a policy to see which carrier offers the best deal for someone in your situation — especially if you have recently experienced a life change that could lead to higher insurance rates.

For example, teenage drivers are more likely to get into car accidents than drivers in any other age group, and they are generally charged more for auto insurance as a result.[3] For this reason, it may be necessary to shop around to prevent or mitigate a burdensome rate hike if you plan to add a child who just turned 16 to your car insurance policy.

For the simplest comparison shopping process possible, consider going through . Once you fill out a short questionnaire, we’ll connect you with insurance agents who can help you compare quotes for various types of policies for free.Click here to select the type of coverage you need and start comparing insurance quotes today!

5. Shop for Discounts

Going into the autumn months, there are several steps you can take to save money on your property and casualty (P&C) insurance policies, including homeowners insurance and auto insurance. Examples of common discounts include the following:

- Bundling: If an insurer offers several different insurance products, you may be able to earn a discount by bundling multiple policies together. For example, you may save money by purchasing home and auto insurance from the same provider.

- Loss prevention: Insurance companies often offer discounts to policyholders who install technology or implement other measures to lower the odds that they will have to file an insurance claim for costly repairs or replacements of damaged or lost items. Loss prevention measures that could lead to discounts include home security systems and anti-theft devices for cars.

- Preferred payment: Many insurance carriers will grant you a discount if you pay your premiums through the insurer’s preferred payment method. This may involve paying your premium for the entire year up front or using an electronic funds transfer (EFT).

- Occupational: You may qualify for an insurance discount based on your profession. For example, some insurance companies offer discounts to military personnel and first responders.

- Loyalty: By staying with the same insurance company for several years, you could eventually qualify for discounted rates and potentially other benefits.

- Claim-free: Insurers often reward low-risk policyholders by offering discounts to those who go an extended period of time without filing any insurance claims.

- New property: It may be cheaper to insure a new car or home than an older one, depending on your insurance company.